About this guide

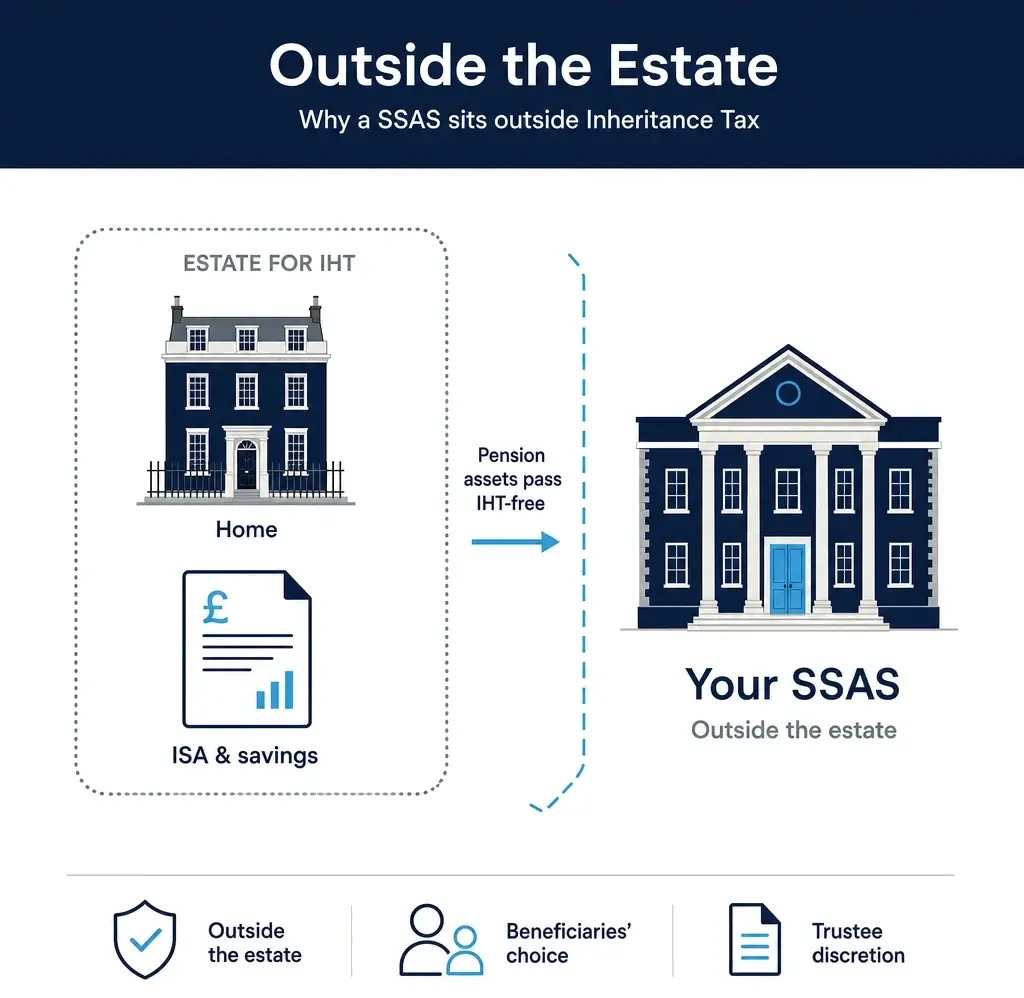

Under current rules (2025/26), unspent SSAS pension funds sit outside the estate for Inheritance Tax purposes — they pass to nominated beneficiaries without IHT. From 6 April 2027, proposed legislation will bring unspent pension funds within the scope of IHT at the standard 40% rate. This guide is for UK company directors with significant SSAS funds who need to understand the current death benefit rules, what is changing and when, and what practical planning options exist before the April 2027 implementation date.

What you'll learn in the SSAS Death Benefits & IHT Guide

- How SSAS death benefits work now. The trust structure that places pension funds outside the estate; the role of the Expression of Wish in guiding trustee discretion; who can be a beneficiary; and the critical age-75 boundary that determines whether benefits pass tax-free or subject to income tax.

- The age-75 boundary explained in full. Before age 75 with an uncrystallised fund: benefits can pass entirely tax-free to beneficiaries. After age 75: income tax at the beneficiary's marginal rate applies when drawn. The Lump Sum and Death Benefit Allowance of £1,073,100 and how it interacts with multiple pension benefits.

- The Expression of Wish: what it is and why keeping it current matters. Why it is non-binding but almost always followed; the life events that make a review essential (marriage, divorce, birth of children, death of a named beneficiary); and how to structure nominations including contingent beneficiaries and generational cascades.

- The April 2027 changes — the full picture. The October 2024 Budget announcement. What “included in the estate for IHT” means in practice for a director with a £1,000,000 SSAS fund. The interaction with the nil-rate band (£325,000), the Residence Nil-Rate Band, and the spousal exemption. The new administrative challenge of co-ordinating IHT calculation across pension and non-pension assets.

- Four planning strategies for directors. Drawdown planning before 2027 to reduce the fund exposed to IHT. Reviewing and restructuring the Expression of Wish in light of the new rules. Spousal planning and the sequencing of pension drawdown. Combining SSAS pension planning with broader estate planning structures such as Family Investment Companies.

- Business continuity: what happens to the SSAS when a member dies. The sole-member scenario — the scheme administrator manages distribution. The multi-member scenario — death of one member does not affect the scheme's continuity. Why multi-member schemes are more resilient.

- The status of the legislation. The April 2027 rules are in draft and subject to consultation. The guide is clear about what is confirmed, what remains uncertain, and where the rules may still change before implementation.

This guide is written for you if…

- You are a UK company director with a substantial SSAS fund — typically £300,000 or more — who has relied on the pension's IHT efficiency as part of your estate planning and needs to understand what is changing

- You have not reviewed your Expression of Wish in more than two years, or your personal circumstances have changed since you last completed it

- You want to understand whether drawdown planning before April 2027 could reduce the IHT exposure on your pension fund

- You are a director of a multi-member SSAS and want to understand what happens to the scheme structure when a member dies

- You are working with a financial adviser or solicitor on estate planning and want a clear summary of the current and proposed pension IHT rules to bring to that conversation

This guide is educational. The April 2027 rules are in draft legislation as of the publication date. Always seek advice from a qualified financial adviser and solicitor before making estate planning decisions.

Straight from the guide

“Under the proposed rules, a director with a SSAS fund of £1,000,000 who dies after April 2027 (and whose estate is above the nil-rate band) could face an IHT charge of up to £400,000 on that pension fund — compared to £0 under current rules.”

“The April 2027 changes create a genuine planning window. Directors who take action before implementation — by reviewing their pension structure, drawdown strategy, and wider estate planning — can position themselves more effectively than those who wait.”

About this guide

Written by SSAS practitioners with over two decades of experience in pension death benefit planning for UK company directors. Published by Holtram TLPI Ltd, HMRC Scheme Administrator (A0140182), operating within The Pensions Regulator's framework. Established 2003.

Questions about this guide

Is this guide really free?

Yes. No payment is required. You submit your email address and receive the guide immediately. You can unsubscribe from follow-up emails at any time.

What happens after I download?

You receive your guide by email within minutes. The follow-up email series covers SSAS fundamentals, tax planning, property investment, and practical guidance on the April 2027 changes.

Will you sell my data?

No. Your details are held by Holtram TLPI Ltd. We do not sell or share personal data with third parties for marketing purposes.

Are the April 2027 IHT changes definitely going ahead?

The October 2024 Budget announced the changes and draft legislation has been published. The direction of travel is clear, but some details — particularly around administration, the spousal exemption mechanics, and the treatment of funds already in drawdown — are still subject to consultation. The guide clearly distinguishes between what is confirmed and what remains uncertain.

Should I start drawing down from my SSAS now to reduce the IHT exposure?

Drawdown planning is one of the strategies discussed in the guide — but it requires careful analysis of your personal tax position, the size of your fund, and your other assets. Drawing down more now means paying more income tax now. Whether the income tax cost is worth the IHT reduction depends on individual circumstances. The guide explains the framework; the calculation requires professional advice.