How to wind up a SSAS

Winding up a SSAS is a formal process that requires careful preparation, trustee consensus, and coordination with your scheme practitioner, HMRC, and The Pensions Regulator. Done correctly, it is a straightforward — if time-consuming — process. Done without proper planning, it can create tax complications and delays that are entirely avoidable.

Winding up a SSAS involves a formal six-step process: a trustee resolution to wind up, notification to The Pensions Regulator, realisation of scheme assets to cash, settlement of all liabilities, preparation of final scheme accounts, and distribution of funds to members (normally as pension benefits or transfer to another registered scheme). The full process typically takes 3–12 months. HMRC deregisters the scheme once all members have received their benefits.

When Might You Wind Up a SSAS?

A SSAS can continue indefinitely — there is no requirement to wind it up unless the trustees choose to do so or circumstances make continuation impractical. Common reasons for winding up include:

- All members have taken their benefits: Once all members have fully crystallised their pension benefits and there are no remaining active members, the scheme has fulfilled its purpose.

- Company dissolution: When the sponsoring employer ceases to trade or is struck off, the scheme loses its sponsoring employer. While the SSAS can technically continue without a sponsoring employer, in practice dissolution often triggers a wind-up.

- Consolidation into a new structure: Some directors wind up an existing SSAS to merge all member benefits into a new, freshly established scheme — for example, to add family members or change practitioners.

- All members prefer individual arrangements: Members may decide they prefer to hold their pension benefits in individual SIPP or drawdown arrangements rather than continuing within a collective trust structure.

- Scheme is no longer cost-effective: For a very small fund, the ongoing administration costs of maintaining a SSAS may outweigh the benefits of continuing the arrangement.

The Wind-Up Process: Step by Step

-

Formal trustee resolution to wind up

The winding-up process begins with a formal resolution passed by all trustees, documented in a trustee minute. The resolution should specify the date from which the winding-up process is to begin and confirm all trustees' consent. This is the trigger document for everything that follows.

-

Notify The Pensions Regulator

The trustees are required to notify The Pensions Regulator (TPR) that the scheme is entering wind-up. Your SSAS practitioner will submit the appropriate notification on the trustees' behalf. TPR requires a Scheme Return to be filed confirming the wind-up decision.

-

Realise and convert assets to cash

All scheme investments must be converted to cash before the scheme can be wound up and deregistered. This is often the most time-consuming stage. Shares are sold through the appropriate market. Property must be sold at market value through a formal disposal process. Loans from the scheme to employers or third parties must be repaid in full — they cannot be written off or transferred in kind without potential tax consequences.

-

Settle all scheme liabilities

Before distributing any funds to members, all outstanding liabilities must be settled: administration fees, professional fees, any VAT obligations, and any outstanding costs incurred during the wind-up process itself. The trustees need to ensure there is nothing outstanding before final distributions are made.

-

Prepare final scheme accounts

Final scheme accounts must be prepared, showing the scheme's financial position at the point of wind-up. These accounts confirm the fund available for distribution to members and serve as the record for HMRC and TPR purposes.

-

Distribute funds to members

Once liabilities are settled, the remaining funds are distributed to members. For uncrystallised funds, members have options: take the pension commencement lump sum and move into drawdown; transfer to another registered pension scheme; or, if eligible for small pots treatment, take the entire remaining balance as a lump sum. The tax treatment depends on which option each member chooses.

-

Submit final returns and deregister with HMRC

Once all funds are distributed, the scheme administrator submits a final Event Report to HMRC and applies for deregistration of the scheme. HMRC confirms deregistration and removes the scheme's HMRC registration number from the register of pension schemes. The scheme formally ceases to exist as a registered pension scheme at this point.

How Long Does Winding Up Take?

The timeline for winding up a SSAS depends primarily on the complexity of the scheme's investments. A simple scheme holding only cash could theoretically be wound up within a few months. A scheme holding commercial property, outstanding loans, and multiple investment accounts will take considerably longer.

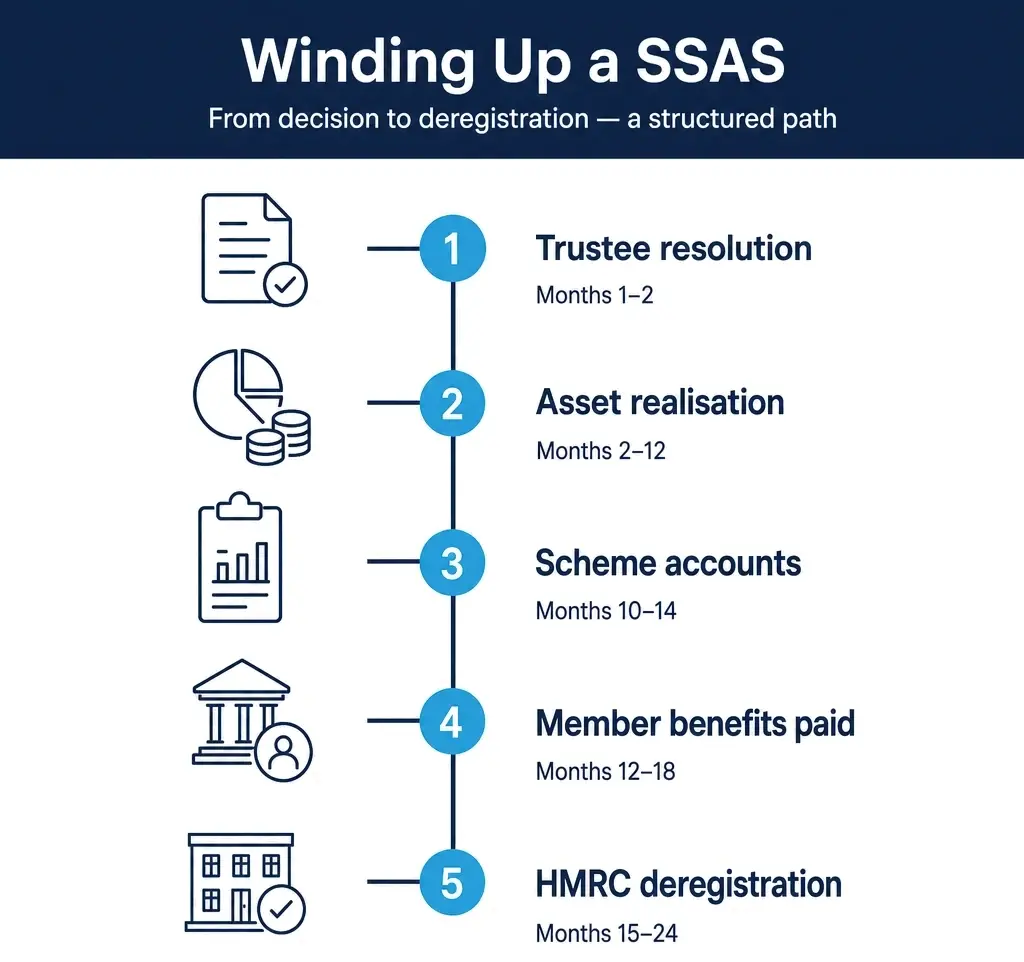

Indicative wind-up timeline

Months 1–2: Trustee resolution, TPR notification, begin asset realisation process

Months 2–12: Property sale (subject to market conditions), loan repayment, investment liquidation

Months 10–14: Final accounts preparation, liability settlement

Months 12–18: Member benefit distribution and transfer processing

Months 15–24: Final HMRC reporting and scheme deregistration

For schemes with commercial property, the largest variable is how quickly the property can be sold at an acceptable price. Trustees should not feel pressured to accept a below-market sale simply to accelerate the wind-up process — the fiduciary duty to act in members' interests applies throughout.

Tax Implications of Winding Up

The tax treatment of distributions during a SSAS wind-up depends on whether a member's benefits are uncrystallised (not yet drawn) or crystallised (already in payment or in drawdown).

| Member's Status | Distribution Type | Tax Treatment |

|---|---|---|

| Under age 57, uncrystallised | Transfer to another scheme | Tax-free transfer (no immediate charge) |

| Age 57+, uncrystallised | PCLS + drawdown designation | 25% PCLS tax-free; remainder taxed as income on withdrawal |

| Already in drawdown | Drawdown fund transfer or encashment | Transfer is tax-free; income withdrawals taxed in the usual way |

| Any age | Trivial commutation (very small funds) | 25% tax-free; 75% subject to Income Tax |

Lump Sum Allowance (LSA) for 2025/26: The total tax-free lump sum a member can take across all their pension arrangements over their lifetime is capped at £268,275 (the Lump Sum Allowance). If a member has already used some of this allowance through previous pension payments, the remaining allowance available at wind-up will be reduced accordingly.

Transferring Out to Another Scheme vs Taking Benefits

Not all members need to take their benefits at wind-up. A member who has not yet reached their normal minimum pension age (currently 55, rising to 57 in April 2028), or who simply prefers to keep their pension savings growing, can transfer their uncrystallised funds to another registered pension scheme — a new SSAS, a SIPP, or an occupational scheme.

Benefits of transferring out

- No immediate tax charge — the transfer is a pension-to-pension movement

- The pension savings continue to grow in a tax-advantaged environment

- The member has time to decide how to take benefits at a point that suits them

Choosing the right receiving scheme

If you are transferring to a new SSAS — for example, a fresh scheme for the next generation of the business — allow sufficient time for the new scheme to be established and registered with HMRC before the wind-up transfers are completed. HMRC registration takes approximately 8–12 weeks and should be initiated well before the wind-up transfers are ready to proceed.

What Happens to Existing Loanbacks During Wind-Up?

A connected loanback — the loan from scheme to the sponsoring employer — cannot simply be written off or forgiven when the scheme is winding up. The loan is a scheme asset that must be realised for the benefit of members.

Options for dealing with an outstanding loanback at wind-up include:

- Full repayment: The employer repays the outstanding loan (capital plus any accrued interest) in full before or during the wind-up process. This is the cleanest outcome.

- Accelerated repayment: If the 5-year repayment schedule means the loan will not be fully repaid before wind-up, the trustees can require early repayment of the remaining balance (the original loan terms typically provide for this).

- Transfer of the loan asset: In some circumstances, the outstanding loan can be transferred to a receiving scheme as part of an in-specie transfer, provided the receiving scheme accepts this and the documentation supports it.

Writing off a loanback is not permitted: Forgiving or writing off a connected loanback during wind-up would be treated by HMRC as an unauthorised payment to the sponsoring employer. This would attract significant tax charges for both the scheme and the employer. Always ensure outstanding loans are handled correctly with professional guidance.

What Happens to Commercial Property Held in the SSAS?

Commercial property held within a SSAS during wind-up must be sold at market value through a formal process. The trustees cannot simply transfer ownership of the property to themselves personally — this would constitute a benefit in kind and could be treated as an unauthorised payment.

The property can be sold to:

- An unconnected third party through the open market

- The sponsoring employer, provided the sale is at full market value as evidenced by an independent valuation

- A member-trustee personally, again only at full independently evidenced market value, and again with potential for scrutiny from HMRC on connected party transactions

An independent RICS-qualified valuation is strongly recommended for any property sale during wind-up, particularly where the buyer has any connection to the scheme. The valuation protects the trustees from claims that they undersold the property at members' expense.

Summary

Winding up a SSAS is a structured, formal process that begins with a trustee resolution and ends with HMRC deregistration. The key steps are: trustee resolution, TPR notification, asset realisation, liability settlement, final accounts, benefit distribution, and HMRC deregistration. The timeline ranges from several months for a simple cash-only scheme to 18–24 months for a scheme with property and outstanding loans. Outstanding loanbacks must be repaid, not written off. Property must be sold at independently evidenced market value. Members can transfer uncrystallised benefits to another registered scheme rather than taking them at wind-up, which is often the most tax-efficient approach for younger members or those who do not need the funds immediately.

Disclaimer: Winding up a registered pension scheme involves complex HMRC reporting and legal obligations. This article is for educational purposes only and does not constitute legal, tax, or financial advice. Always engage your SSAS practitioner and, where appropriate, a solicitor before initiating the wind-up of a SSAS.