How drawdown from a SSAS works

Building up a substantial SSAS pension fund is only half the picture. Understanding how and when you can access those funds — and what tax applies — is equally important when planning your retirement finances. This guide explains the SSAS drawdown rules in plain terms, covering access ages, tax-free cash, flexi-access drawdown, phased crystallisation, and the interaction between drawing benefits and continuing to contribute.

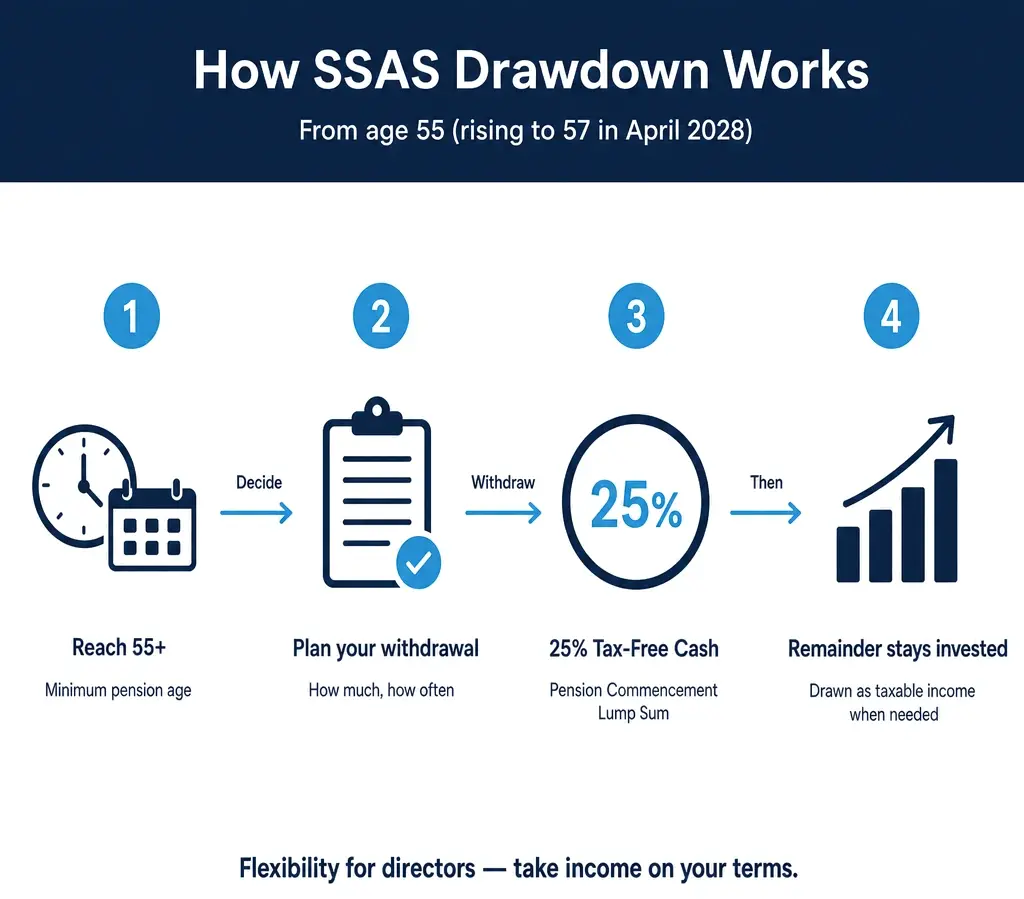

SSAS members can access their pension from age 55 (rising to 57 on 6 April 2028, per PTM062100). Up to 25% of crystallised funds can be taken as a tax-free lump sum (capped at the £268,275 Lump Sum Allowance). The remainder stays invested inside the SSAS and can be drawn as flexible income — called flexi-access drawdown — taxed as income at the member’s marginal rate. SSAS does not require annuity purchase; members can remain in drawdown indefinitely.

When Can You Access Your SSAS?

The normal minimum pension age (NMPA) — the earliest age at which you can access your SSAS benefits — is currently 55. This applies to benefits taken on or after 6 April 2010.

The government has announced that the NMPA will increase to 57 on 6 April 2028. After that date, most individuals will need to be at least 57 before they can access their pension. There is a transitional period and some protections may apply to individuals who had a right to take benefits before age 57 under their scheme rules before a certain date — but for the majority of SSAS members setting up new arrangements today, 57 will be the effective minimum access age from 2028 onwards.

Note on the 2028 Change: If you are currently between 55 and 57 and plan to access benefits, it is worth checking whether the transitional protections apply to you. The rules here are nuanced and speak to your SSAS scheme administrator to confirm how the transitional provisions apply. For those who are currently under 55, the age 57 minimum from 2028 will almost certainly apply by the time they are eligible to draw benefits.

How does the 25% tax-free lump sum work in a SSAS?

When you crystallise your SSAS pension — the technical term for moving from the accumulation phase into benefit — you are entitled to take a tax-free lump sum of up to 25% of the funds you are crystallising. This is formally called a pension commencement lump sum (PCLS).

Since April 2024 and the abolition of the Lifetime Allowance, the maximum tax-free lump sum you can take across all your pension arrangements in your lifetime is capped at £268,275 (the Lump Sum Allowance for 2025/26). Any PCLS you take reduces this lifetime limit.

If your SSAS fund is £500,000, for example, crystallising the full fund would entitle you to a tax-free lump sum of up to £125,000 (25% of £500,000) — well within the £268,275 cap. If your fund were £1.5 million, 25% would be £375,000, but you would only receive £268,275 tax-free; the remaining £106,725 would be subject to Income Tax at your marginal rate if taken as a lump sum, or you would simply take a lower PCLS.

It is important to note that you do not have to take the full 25% tax-free cash in one go. Phased crystallisation (described below) allows you to take tax-free cash gradually over time, alongside an ongoing income from the crystallised portion.

What is flexi-access drawdown in a SSAS?

Flexi-access drawdown is the most common way that SSAS members take income from their pension. After crystallising your funds (and taking any tax-free cash), the remainder of your fund stays invested within the scheme and you can withdraw income from it at whatever level you choose — monthly, quarterly, annually, or in ad hoc amounts.

All income taken from flexi-access drawdown is subject to Income Tax at your marginal rate. This means:

- Drawdown income is treated as earned income in the year you receive it

- It is added to any other taxable income you have — salary, dividends, rental income, state pension — and taxed accordingly

- You will receive a personal allowance (currently £12,570 for most people) before Income Tax applies, but this may already be used up by other income

There is no minimum or maximum income level for flexi-access drawdown — you can take as much or as little as you like, whenever you like. This flexibility is one of the key advantages of a SSAS over a traditional annuity.

Key Point: Funds Remain Invested

In flexi-access drawdown, the portion of your SSAS that has not yet been withdrawn remains invested within the scheme, continuing to benefit from tax-free investment growth. You are not required to withdraw all your funds at once — the drawdown phase can last for the rest of your life.

What is phased drawdown and how does it work?

Phased drawdown (sometimes called phased crystallisation) is a particularly powerful feature of a SSAS for directors who want to draw income gradually while keeping as much of their fund as possible growing in the tax-efficient pension environment.

Instead of crystallising your entire SSAS fund at once, you can crystallise it in stages — perhaps 10% or 20% of the fund each year. Each time you crystallise a tranche:

- You can take up to 25% of that tranche as tax-free cash (subject to the £268,275 lifetime cap)

- The remaining 75% enters flexi-access drawdown

- The uncrystallised portion continues to grow tax-free within the scheme

This approach can be highly tax-efficient, particularly for directors who have income from other sources in some years but lower income in others. By crystallising more in lower-income years, you can potentially draw benefits at a lower marginal tax rate.

Illustrative Example

Phased Drawdown Strategy

A director retires at 60 with a SSAS fund of £800,000. Rather than crystallising everything at once, they choose to crystallise £100,000 per year for the first four years.

Year 1: Crystallise £100,000. Take £25,000 as tax-free cash. Place £75,000 into flexi-access drawdown. Draw £30,000 from drawdown. Income tax applies to the £30,000 at their marginal rate. The remaining £700,000 continues growing tax-free.

This approach spreads tax-free cash entitlement over time and gives flexibility to adjust annual income based on other income sources. Total tax-free cash over four years in this example: up to £100,000 (25% of £400,000 crystallised). This is illustrative; tax outcomes depend on individual circumstances.

Can I take SSAS benefits while still contributing?

It is possible to be both drawing benefits from your SSAS and still making contributions to it — but there are significant rules governing how this works.

Once you begin taking income from flexi-access drawdown, the Money Purchase Annual Allowance (MPAA) is triggered. From that point on, your maximum contribution to any money purchase pension scheme (including your SSAS) is reduced to £10,000 per year — not the standard £60,000.

This means:

- If you plan to continue making significant pension contributions after retirement, triggering flexi-access drawdown early can severely limit your ability to do so

- Taking your 25% tax-free cash without also drawing drawdown income does not trigger the MPAA — you can take the lump sum while leaving the remaining fund uncrystallised, and continue contributing at the full £60,000 level

- Carrying on as a working director-shareholder while drawing from your SSAS is perfectly possible, but the interaction between contribution levels and benefit crystallisation needs careful planning

What other options exist for taking SSAS benefits?

Uncrystallised funds pension lump sum (UFPLS)

A UFPLS allows you to take a lump sum directly from uncrystallised funds — without formally entering drawdown. Twenty-five percent of each UFPLS payment is tax-free; the remaining 75% is subject to Income Tax. This is an alternative to taking a PCLS and entering drawdown, and can be flexible for directors who want occasional lump sum payments rather than regular income.

However, taking a UFPLS does trigger the MPAA, so the same contribution restrictions apply.

Annuity purchase

You can use funds from your SSAS to purchase an annuity from an insurance company. An annuity converts your pension fund into a guaranteed income for life (or a fixed term). Annuity rates have improved significantly since 2022 and may be worth considering for a portion of your fund, particularly if you want the certainty of a guaranteed income alongside flexible drawdown for the remainder.

Purchasing a standard annuity does not trigger the MPAA, though a flexible (investment-linked) annuity where income can decrease does.

Serious ill-health lump sum

If you are diagnosed with a terminal illness or a condition that is expected to significantly shorten your life, you may be able to take your entire SSAS fund as a lump sum before age 57. Specific HMRC criteria apply. If taken before age 75, serious ill-health lump sums may be paid tax-free (subject to the Lump Sum and Death Benefit Allowance). After 75, they are subject to Income Tax.

Summary: SSAS Drawdown Options at a Glance

| Access method | Tax treatment | Triggers MPAA? |

|---|---|---|

| PCLS (tax-free cash lump sum) | Tax-free up to £268,275 lifetime cap | No (alone) |

| Flexi-access drawdown income | Income tax at marginal rate | Yes |

| Uncrystallised funds pension lump sum (UFPLS) | 25% tax-free; 75% taxable at marginal rate | Yes |

| Annuity (standard) | Income tax at marginal rate | No |

| Serious ill-health lump sum (pre-75) | Tax-free (subject to LSDBA limit) | Yes |

Disclaimer: This article is for educational purposes only and does not constitute financial advice. SSAS pensions are corporate pension schemes registered with HMRC and overseen by The Pensions Regulator (TPR), and do not require FCA regulation. Tax rules are subject to change and depend on individual circumstances. The information in this article is based on our understanding of HMRC rules for the 2025/26 tax year.