How to transfer a pension into a SSAS

If you are setting up a SSAS or already have one established, consolidating your existing pensions into the scheme can significantly increase the fund available for investment. This guide explains which pension types can be transferred, which cannot, and takes you through the transfer process step by step.

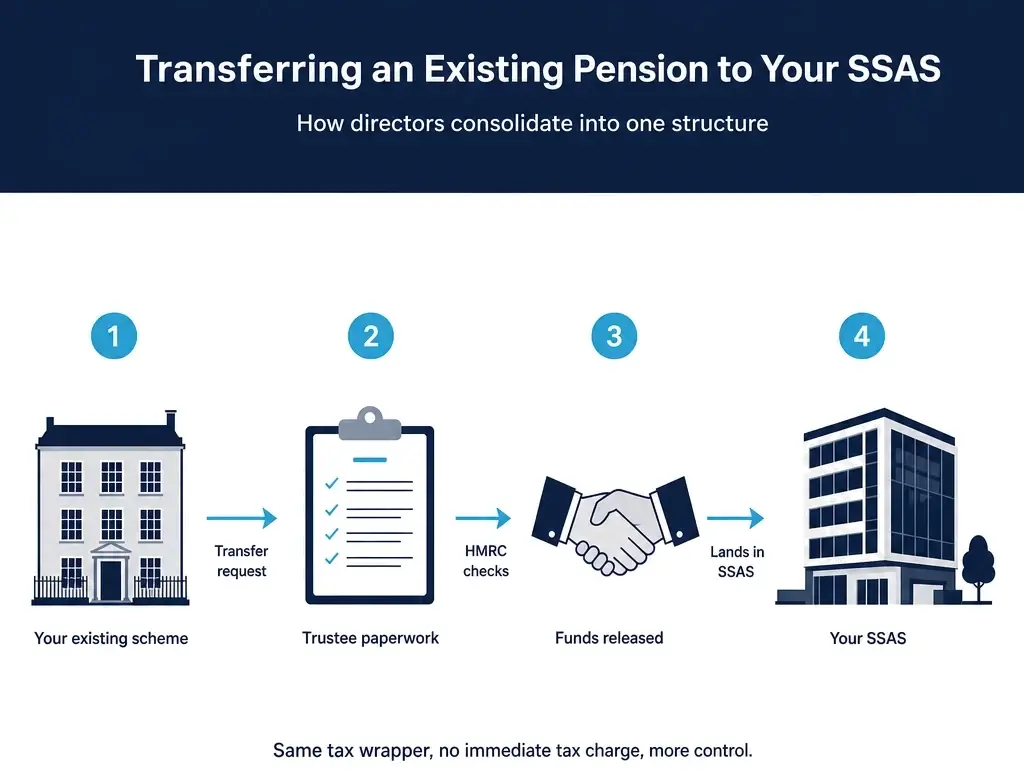

Transferring an existing pension into a SSAS typically takes 4–12 weeks: the new SSAS administrator handles HMRC paperwork, the receiving scheme valuations, and trustee resolutions. Defined-contribution pensions transfer straightforwardly; defined-benefit transfers above £30,000 require FCA-regulated advice. Most transfers complete without tax charge, but lifetime allowance considerations may apply for large transfers.

Last updated: June 2026 · 10 min read · UK 2026/27 tax year

Which Pensions Can Be Transferred into a SSAS?

Most types of defined contribution pension can be transferred into a SSAS, provided the transfer is handled correctly and HMRC's rules are followed throughout.

Personal pensions

Standard personal pensions — those arranged individually with an insurance company or pension provider — can be transferred into a SSAS. These are sometimes called "stakeholder pensions" if they were set up under that framework. The transfer is straightforward: your existing provider will need to calculate the current transfer value and pass the assets to the SSAS.

SIPPs (Self-Invested Personal Pensions)

A SIPP can be transferred into a SSAS in full or in part, depending on the SIPP provider's rules. If your SIPP currently holds direct investments such as shares or property, those assets may need to be liquidated before transfer, or — in some cases — transferred in specie (as existing assets rather than cash). Discuss the specifics with your SSAS practitioner before initiating a SIPP transfer that holds non-cash assets.

Workplace defined contribution pensions

Defined contribution (DC) workplace pensions — including group personal pensions and occupational money purchase schemes from previous employers — can generally be transferred into a SSAS. These are common for directors who have accumulated pension pots from earlier employment before starting their own company.

Other SSAS schemes

If you hold membership in another SSAS — for example, from a previous business — those funds can be transferred across to your current SSAS, subject to trustee consent and scheme rules at both ends.

Pension credit following divorce

A pension credit awarded through a pension sharing order on divorce can, in some circumstances, be transferred into a SSAS. This requires specialist advice and the agreement of the scheme trustees.

Which Pensions Cannot Be Transferred?

The State Pension

The State Pension cannot be transferred into any private pension arrangement. It is a government benefit, not a pension fund, and has no transfer value. Your entitlement to State Pension is entirely separate from your SSAS.

Defined benefit pensions (DB pensions)

Defined benefit — also called "final salary" — pensions can technically be transferred into a SSAS, but this is a high-risk area requiring careful consideration. Under FCA rules, if the transfer value is £30,000 or more, you are legally required to take regulated financial advice from a specialist adviser before the transfer can proceed. This is a consumer protection measure because defined benefit pensions offer guaranteed income for life, and giving up that guarantee is not appropriate for everyone. Do not attempt to transfer a DB pension without first taking independent regulated advice.

Important: Defined benefit pension transfers require regulated financial advice where the transfer value is £30,000 or more. This is a legal requirement, not a formality. Only proceed once you have received and understood a written recommendation from an FCA-authorised pension transfer specialist.

Unfunded public sector pensions

Some public sector pensions — for example, NHS, teacher, and civil service schemes — are unfunded. These cannot be transferred out at all. If you previously worked in the public sector, check whether your pension is funded or unfunded before making any assumptions.

Annuities already in payment

Once a pension has been converted into an annuity and income is in payment, the arrangement is fixed. Annuities cannot be transferred back into a SSAS or any other pension scheme.

The Transfer Process: Step by Step

Transferring a pension into a SSAS involves coordination between you, your SSAS practitioner, and the ceding scheme (the pension you are moving from). Here is what the process typically looks like.

-

Establish your SSAS and receive your HMRC registration number. Pension transfers cannot proceed until the SSAS is fully registered with HMRC. Your scheme practitioner will handle registration, which typically takes 8–12 weeks.

-

Obtain transfer value statements from each ceding scheme. Contact each pension provider whose funds you wish to transfer and request a Cash Equivalent Transfer Value (CETV) statement. This tells you the current value of the fund on a specific date.

-

Check for exit charges or market value reductions. Some older pension contracts impose exit penalties if you transfer before a certain date or age. These are called Market Value Reductions (MVRs) on with-profits funds. Factor these into your decision before proceeding.

-

Confirm safeguarded benefits. If any pension includes guaranteed annuity rates (GARs) or other safeguarded benefits, regulated advice is required regardless of the transfer value. Do not waive these benefits without fully understanding what you are giving up.

-

Complete transfer discharge forms. Your SSAS practitioner will supply the necessary paperwork for the ceding scheme. Both the SSAS trustee details and the HMRC scheme registration number will be required to authenticate the receiving scheme.

-

The ceding scheme sends funds to the SSAS bank account. Transfers are typically completed by BACS or CHAPS payment. The funds arrive as cash into the SSAS bank account, at which point the trustees can invest them according to the scheme's investment strategy.

-

Update your SSAS records. Your scheme administrator will update the member's accrued benefits record to reflect the transferred-in funds. These are recorded as uncrystallised funds and count towards your pension lifetime position.

How Long Do Pension Transfers Take?

Transfer timescales vary considerably depending on the type of pension being transferred and the responsiveness of the ceding scheme.

| Pension Type | Typical Transfer Time | Notes |

|---|---|---|

| Personal pension (cash) | 4–8 weeks | Usually straightforward |

| SIPP (cash only) | 6–10 weeks | Depends on provider |

| SIPP (in specie) | 10–20 weeks | Asset transfers are more complex |

| Workplace DC pension | 8–12 weeks | Employer/trustee sign-off sometimes needed |

| Defined benefit pension | 3–6 months | Regulated advice process adds time |

The Financial Conduct Authority requires ceding schemes to complete transfers within six months. In practice, most complete much faster, but delays can occur when documentation is incomplete or the ceding scheme raises queries. Chase proactively if a transfer is taking longer than expected.

What Happens to Your Existing Investments During a Transfer?

When you request a transfer, the ceding scheme will typically sell your investments and remit the cash value to your SSAS. This is called a "cash transfer." There are two important implications:

Timing risk: If markets move between the date the CETV was calculated and the date the transfer completes, the actual cash received may differ from the quoted value. This is a normal feature of cash transfers and not something your SSAS practitioner can control.

In specie transfers: In limited circumstances, some assets can be transferred "in specie" — meaning the actual holding is moved across rather than being sold. This is most common with SIPPs holding listed shares. In specie transfers are more administratively complex and not all SSAS practitioners support them for all asset types.

Within HMRC rules: All pension transfers must be genuine transfers for pension purposes. Transfers that are structured to manipulate tax reliefs may be treated as unauthorised payments and attract significant charges. A reputable SSAS practitioner will ensure all transfers are structured correctly.

The Benefits of Pension Consolidation

Many company directors accumulate a collection of small pension pots from previous employment, old SIPPs, and personal pensions over the course of their career. Consolidating these into a single SSAS can offer several practical advantages.

A larger investment fund

The most direct benefit: pooling multiple smaller pots into a single fund creates a larger capital base. This matters particularly for commercial property investment — purchasing property through a SSAS typically requires a minimum fund size to make the numbers work, and consolidation could help you reach that threshold sooner.

Simpler administration

Managing one pension scheme is considerably simpler than tracking multiple providers, statements, and investment platforms. Consolidation reduces the administrative burden and gives you a clearer picture of your overall pension position.

Greater investment flexibility

Individual pension pots held at external providers may be invested in limited fund ranges or with limited flexibility. Once within a SSAS, the trustees have full control over the investment strategy, within HMRC's permitted investment parameters.

Potential cost savings

Running multiple pension arrangements typically means paying multiple annual charges. While a SSAS has its own administration costs, there could be overall savings from eliminating legacy provider fees — particularly on smaller, older pots with high annual charges.

Things to Watch For

Exit penalties on old pensions

Older personal pension contracts — particularly those sold in the 1990s and early 2000s — sometimes included penalties for early transfer. Check the terms of each pension carefully before initiating a transfer. Your SSAS practitioner can help you assess whether the consolidation benefits outweigh any exit costs.

Guaranteed Annuity Rates (GARs)

Some older personal pensions include guaranteed annuity rates — the right to convert your fund into an annuity at a rate significantly better than the open market. These can be extremely valuable and should not be given up lightly. Transferring a pension with a GAR forfeits the guarantee permanently. Regulated advice is required before doing so.

Lifetime allowance position

The Lifetime Allowance (LTA) was abolished from April 2024, but pension savings interact with the Lump Sum Allowance (LSA) and Lump Sum and Death Benefit Allowance (LSDBA) for 2025/26. A large incoming transfer does not itself create a tax charge, but it does affect your available allowances when you come to take benefits. If your total pension savings are substantial, seek advice on your position.

Transfers from pension sharing orders

If a pension credit arises from divorce proceedings, the mechanics of transfer are more complex and time-sensitive. Always involve your SSAS practitioner from the outset if pension sharing orders are involved.

Summary

Transferring existing pensions into your SSAS is one of the most effective ways to build the fund available for investment. Workplace DC pensions, SIPPs, and personal pensions can all be transferred in, typically as a cash transfer following a straightforward discharge process. Defined benefit pensions require regulated advice before any transfer, and unfunded public sector pensions and annuities already in payment cannot be transferred at all. Work with your SSAS practitioner to sequence transfers correctly and ensure all documentation is complete before initiating the process.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Pension transfers, particularly from defined benefit schemes, involve complex considerations. Always seek appropriate professional advice before making transfer decisions.