About this guide

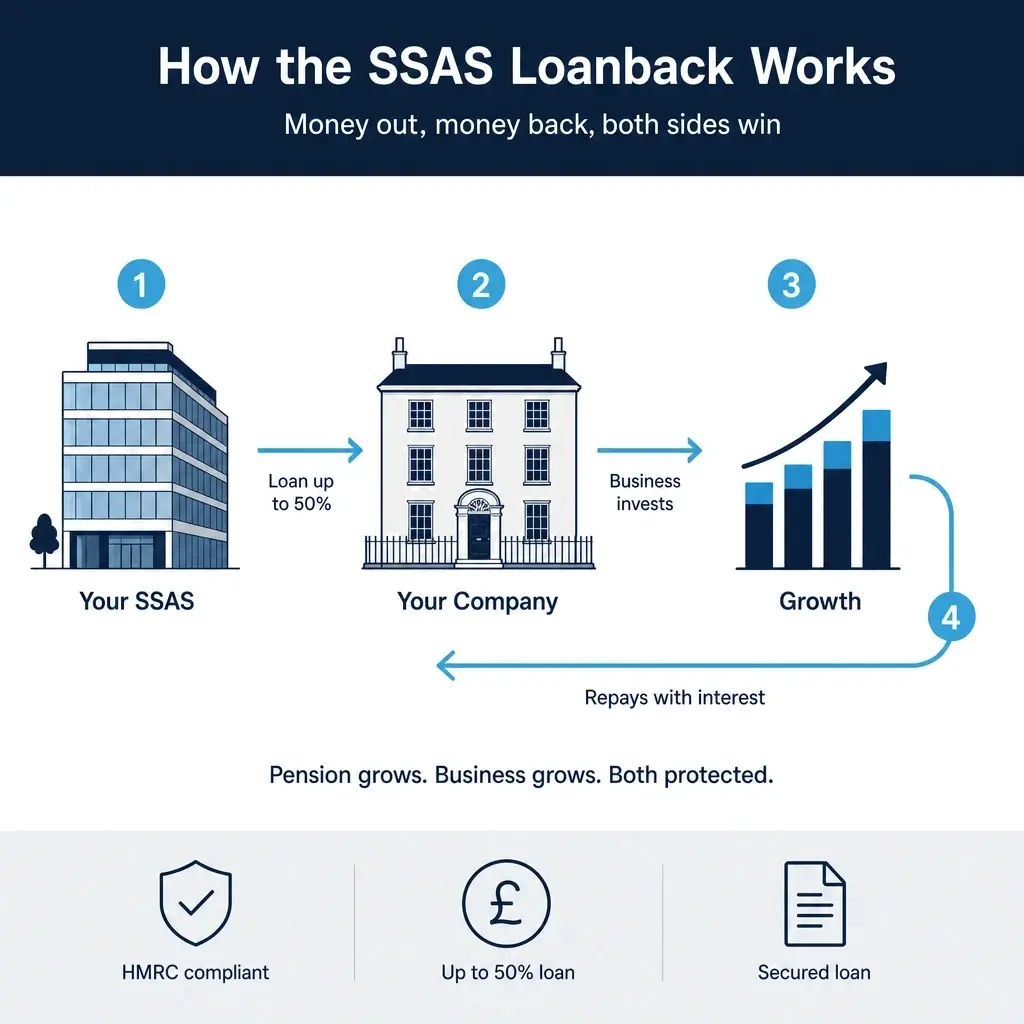

The SSAS loanback is a facility that allows a Small Self-Administered Scheme to lend up to 50% of its net assets to the company that sponsors the scheme — providing business capital from pension funds that have already received Corporation Tax relief. This guide is for UK company directors who want to understand exactly how the loanback works, what HMRC requires, and how the transaction is structured from initial assessment to completion. No other mainstream UK pension structure offers this capability.

What you'll learn in The SSAS Loanback Playbook

- What the loanback actually is. The fundamental logic: company contributes to pension (with CT relief), pension lends back to company, company repays with interest, interest grows the pension fund. The cycle explained step by step — and why it is unique to the SSAS.

- The five HMRC rules — every one must be met. Maximum 50% of scheme net asset value. Maximum five-year term. First-charge security over assets worth at least the loan amount. Interest at no less than 1% above the HMRC official rate (currently 3.25% per annum). Loan to the sponsoring employer only — never to individual members personally.

- The five-step setup process. How to move from initial assessment through security identification, loan agreement drafting, charge registration, and drawdown — with the role of the scheme administrator at each stage.

- What the loan can be used for. Any legitimate business purpose: expansion, property purchase, working capital, equipment, debt refinancing, acquisition. The guide is clear that funds cannot be passed to individual directors as personal income.

- A worked example with full figures. A logistics company director with a £500,000 SSAS borrows £200,000 over five years at 3.25% per annum. A year-by-year repayment schedule shows exactly what flows back into the pension fund — £219,500 in total (capital plus interest).

- Risks and honest considerations. The company must have genuine repayment capacity. Security must hold its value. Documentation must be legally watertight. And the pension fund is exposed to company risk when a loanback is in place — 50% of retirement savings are effectively linked to the business.

- Loanback vs alternative business financing. A comparison table showing bank loans (typically 6–10%), SSAS loanback (minimum 3.25%, interest flowing back to your own pension), director's loans, asset finance, and equity. The case for and against each.

This guide is written for you if…

- You are a UK company director with an existing or planned SSAS and you are considering borrowing from the pension to fund business operations, a property purchase, expansion, or working capital

- Your business needs capital and you want to understand all your options — including whether the loanback is cheaper and more tax-efficient than a bank loan

- You have heard about the SSAS loanback but want to understand the HMRC rules in detail before proceeding, so you know what questions to ask your administrator

- Your SSAS fund has reached a size (typically £100,000+) where a meaningful loan is possible and the cost of setup is proportionate

This guide is not appropriate for directors who have not yet established a SSAS, as the loanback is only available within an existing SSAS trust. It is educational and does not constitute financial or legal advice.

Straight from the guide

“If your SSAS is worth £400,000, the maximum loan is £200,000. This 50% limit applies to the combined outstanding loan balance, not each individual loan.”

“The loanback's advantage is not just the interest rate — it is that the interest payments flow back into your own pension fund. Money that would have gone to a bank as interest cost instead compounds inside your retirement savings.”

About this guide

Written by SSAS practitioners with over two decades of experience administering loanback transactions for UK company directors. Published by Holtram TLPI Ltd, HMRC Scheme Administrator (A0140182), operating within The Pensions Regulator's framework. Established 2003.

Questions about this guide

Is this guide really free?

Yes. No payment is required. Download is immediate on submitting your email address. You can unsubscribe from follow-up emails at any time.

What happens after I download?

You will receive your guide within minutes by email. The follow-up email series covers SSAS fundamentals, property investment, tax planning, and the April 2027 IHT changes.

Will you sell my data?

No. Your details are held by Holtram TLPI Ltd and used only for the purposes described. We do not share personal data with third parties for marketing purposes.

Can I use the loanback for any business purpose?

Yes — any legitimate business purpose. The guide covers common uses including business expansion, working capital, property, equipment, and debt refinancing. The constraint is that the funds must be used by the company (the sponsoring employer), not paid to individual directors as personal income.

What happens if my company can't repay the loan on time?

The outstanding balance risks becoming an “unauthorised payment” under HMRC rules, which triggers a Scheme Sanction Charge of up to 40% of the outstanding amount. This is the most serious risk of the loanback and is covered in detail in the guide. The guide strongly recommends that directors only proceed when genuine repayment capacity exists.